A “slight” adjustment in the wealth tax rate: what impact for your non-profit organisation?

— Other — 3 minutes read

By Antoine Druetz, Partner, Valérie Havaux, Senior Counsel, and Pauline Vansteenkiste, Junior Associate at EY Law.

The “wealth tax”, also referred to as the “tax to reimburse inheritance tax” (“taxe compensatoire des droits de succession” in French and “taks tot vergoeding der successierechten” in Dutch), is an annual tax for non-profit organizations, including international non-profit associations and private foundations (hereafter referred to as “NPOs”).The new law of December 28, 2023, containing various tax provisions, has increased the applicable wealth tax rate, with a notable impact for NPOs which shall not be underestimated.

1) The main changes of the new legislation

Before the reform, NPOs owning more than 25,000 EUR in assets were annually taxed at a 0.17% flat rate on specific tangible assets (such as real estate and cash investments) and intangible assets (such as trademarks and copyrights).

Under the new legislation, instead of a flat tax rate of 0.17%, a progressive ascending rate will be applied, based on the value of the NPO’s eligible taxable assets:

2) The impact on your NPO

As is clear from the above table, this mainly leads to two conclusions:

1. The number of NPOs that remains under the surface increases: the exemption threshold has now been doubled (from 25,000 EUR to 50,000 EUR). However, the fact that an NPO is exempted from the wealth tax does not exempt it from filing a tax return each year; and

2. The “wealthier” NPOs face almost triple the amount of wealth tax that will have to be paid. The practical impact of this reform is illustrated with a number of examples in the below table:

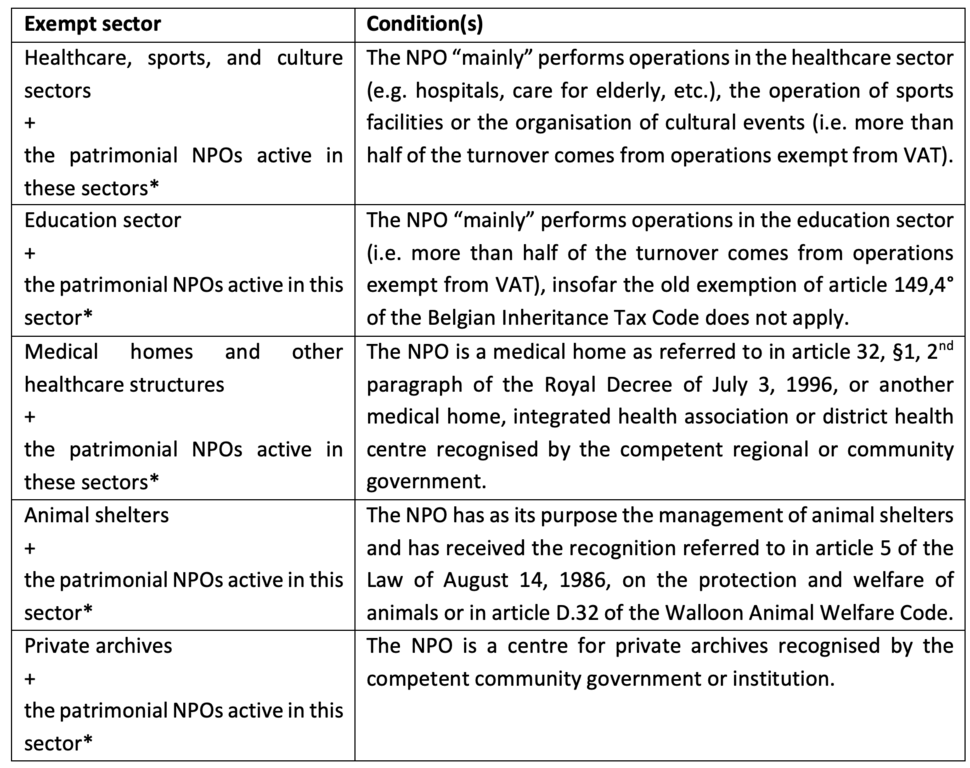

3) Exceptions contained in the new legislation

The rate increase of the wealth tax goes hand in hand with a longer list of exceptions than before. The following sectors fall outside the scope or are now neutralised (and thus still pay a maximum of only 0.17% in taxes) under one or more conditions:

*The rate increase also does not apply to so-called “patrimonial” NPOs which are active in the abovementioned sectors. These are NPOs of which the assets are used for at least 75% by another NPO for the realisation of transactions that can benefit from the VAT exemption referred to above (e.g., an NPO that owns real estate that is being made available to another NPO operating in the healthcare sector).

It is worth noting that foundations of public utility (“Fondations d’utilité publique” in French and “Stichtingen van openbaar nut” in Dutch) are also exempted from this annual tax. As a result, some larger NPOs decide to shelter their (real estate) assets in a foundation of public utility in order to avoid the wealth tax.

4) Entry into force of these changes

Account will be taken of the total assets on January 1, 2024. This implies that the progressive system will already apply to the tax returns that must be submitted by March 31, 2024, at the latest.

5) Conclusion

Although the rate for the “wealthier” NPOs (i.e., with more than 500,000 EUR in assets) within the new progressive system “only” increases from 0.17 % to 0.45 %, this can lead up to a tripling of the taxes to be paid.